How to Finance a Condo in Walnut Creek (2025 Buyer’s Guide)

So you've found the perfect condo in Walnut Creek—now how do you pay for it?

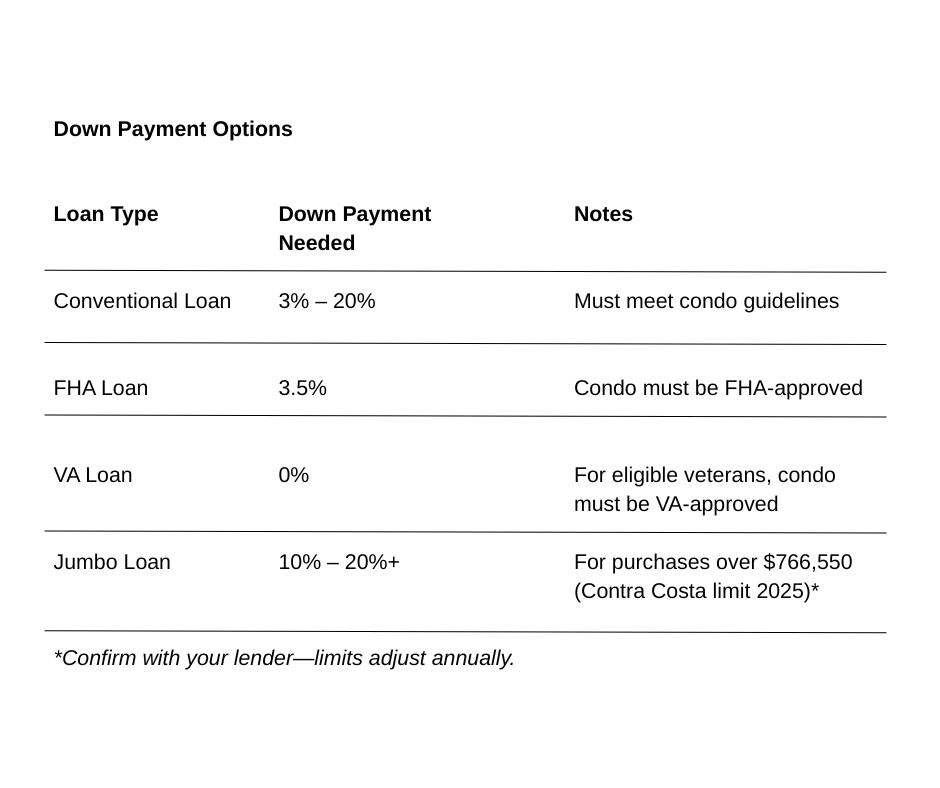

Financing a condo is similar to buying a single-family home in many ways, but there are a few important extra steps and potential challenges that you need to know before you get too deep into the process.

In this post, we’ll break down everything you need to know about mortgages, down payments, loan types, and HOA-related hurdles specific to condos in Walnut Creek.

🏦 Condo Financing vs. Single-Family Homes: What’s Different?

The biggest difference? Lenders look at both YOU and the building.

In a typical home loan, the bank reviews:

Your credit

Your income

Your debt-to-income ratio

With a condo loan, lenders also evaluate:

The building’s financial health (HOA)

The occupancy rate (how many units are owner-occupied)

Whether the building is on a “warrantable” list (more on that below)

🔍 What Makes a Condo “Warrantable” or “Non-Warrantable”?

A warrantable condo is one that meets Fannie Mae or Freddie Mac’s lending guidelines.

That means:

50%+ of units are owner-occupied

No ongoing litigation against the HOA

No single entity owns more than 10% of units

HOA has adequate reserves and budget

The majority of income is from regular HOA dues—not rentals or businesses

A non-warrantable condo may still be financed—but you’ll likely need a larger down payment, higher interest rate, or portfolio lender.

🧠 Pro Tip: Many Walnut Creek complexes—like 555 YVR and The Keys—fluctuate in and out of warrantable status. I work with lenders who stay up to date on these lists.

📝 Documents You’ll Need for Financing

In addition to standard loan documents, your lender may request:

HOA budget & reserve study

Insurance certificates

Master CC&Rs (rules & restrictions)

Condo questionnaire from the HOA

Lenders use these to ensure the building isn’t financially risky.

🏢 FHA- and VA-Approved Condo Complexes in Walnut Creek

As of 2025, these are some communities that may be approved (subject to change):

Skyline

Ygnacio Terrace

Check the FHA Approved Condo List

Check VA Approval Status

🤝 Tips for a Smooth Condo Financing Experience

Get pre-approved with a lender familiar with Walnut Creek condos

Ask your agent (like me!) to check warrantability before making an offer

Review HOA docs early in the escrow process

Avoid surprises by budgeting for HOA fees in your monthly payments

Work with a lender who can fund non-warrantable condos if needed

🔗 Related Posts

📩 Need Help Getting Pre-Approved?

I work with lenders who specialize in financing Walnut Creek condos—even in buildings that aren’t FHA-approved or have tricky HOAs. Let me connect you with the right professionals so your purchase is smooth and successful.

📞 Contact me today for lender referrals and available condo listings

💼 Start your financing plan now and get ahead of the market